Villages of LaiʻŌpua Village 4

Aloha! If you are reading this, it means you have been invited to a lot selection orientation for the Villages of LaiʻŌpua, Village 4. This guide will walk you through everything you need to know — in plain, simple language.

What is this project?

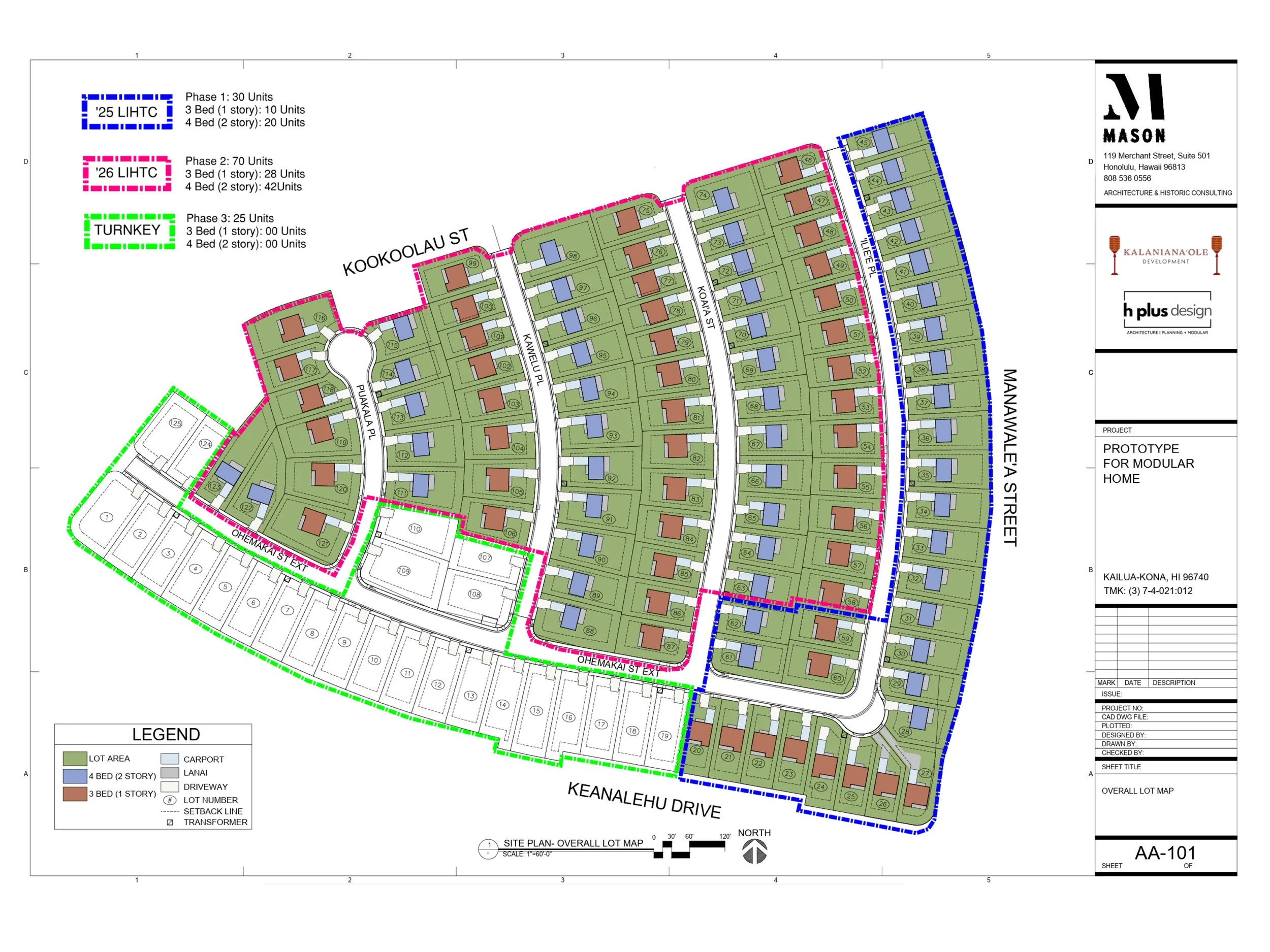

The Department of Hawaiian Home Lands (DHHL) is building 125 new homes in Kailua-Kona on Hawaiian Home Lands. These homes are for Native Hawaiian beneficiaries who are on the DHHL residential waitlist for Hawaiʻi Island.

The 125 lots are split into three groups:

Rent first, buy later

Rent first, buy later

No income limit

100 of these lots use a program called RWOTP. The other 25 are for beneficiaries who want to own their home right away.

What does RWOTP mean?

RWOTP stands for Rent-With-Option-To-Purchase. Here is the simple version:

Then you get the chance to buy that home and become a homeowner on Hawaiian Home Lands.

Think of it like a long test drive. You live in the home, you take care of it, you make it yours. And when the time comes, you have the option to purchase it at a price that is designed to be affordable for your income level.

Why did DHHL choose this approach?

Not every family is ready for a mortgage on Day 1. Maybe you need time to build credit, save money, or just get settled. RWOTP lets you:

Move in sooner — You don't need a mortgage to get started.

Pay what you can afford — Rent is based on your income, not market rates.

Prepare for ownership — 15 years to build stability before you buy.

Stay on DHHL land — Your family on Hawaiian Home Lands, building a future.

This approach was chosen after looking at other options (self-help building, Habitat for Humanity, owner-builder). RWOTP was selected because it serves the most families across all income levels at the same time, with the least risk to you.

What are the homes like?

The RWOTP homes are brand-new single-family houses. There are two sizes:

3-Bedroom / 2-Bath

Approximately 1,150 square feet

Good for smaller families

4-Bedroom / 3-Bath

Approximately 1,425 square feet

Good for larger families

All homes are on DHHL trust land, which means no property tax — not during the rental period and not after you buy.

How RWOTP Works Step by Step

The Big Picture

Here is what happens over time. There are three main phases:

Phase 1: Construction (2026–2027)

First, the homes need to be built. You are selected for your lot before construction starts. The builder (Nan Inc.) will construct all 30 Phase 1 homes over about 12 months.

During this time, you do not need to do anything. Just wait for your home to be ready.

Phase 2: You Are a Renter (Years 1–15)

Once your home is complete, you move in and sign a rental agreement. Here is what life looks like during the rental period:

Your rent is affordable. It is set based on your income level, not what the market charges. Monthly rents range from about $716 to $1,747 depending on your income tier and bedroom count.

Every year, your income is checked. A third-party company will verify your household income each year. This is required by the federal programs (LIHTC and NAHASDA) that help pay for building the homes. This is normal — it is not a test you can fail. It just confirms your rent is set at the right level.

The home is professionally managed. A property management company handles maintenance and repairs during this period. You are responsible for keeping the home clean and in good shape, like any rental.

What you cannot do during this period: You cannot add an ADU (additional dwelling unit), make major structural changes, or sublet the home. These rules come from the federal funding programs, not from DHHL.

Phase 3: You Become a Homeowner (Year 16+)

This is the moment everything has been building toward.

At Year 16, you get the option to purchase your home. The price will be set at a level that is designed to be affordable based on the income tier of your lot.

When you purchase, here is what happens:

You get your 65-year DHHL homestead lease

This is the standard Hawaiian Home Lands lease. The land stays in the DHHL trust (as required by law), and you lease it for 65 years.

You own the home itself

The house, the improvements, everything above the ground — that is yours. You own it outright.

You can improve your property

Once you own, you can add an ADU, renovate, expand — the home is yours to build on. You start building real equity.

What if I am not ready to buy at Year 16?

That is completely okay. The purchase is an option, not a requirement. If you are not ready, you can continue renting. Nobody will force you to buy or move out. You can try again later when your situation allows.

Income Limits & Eligibility

What is AMI?

You will hear the term "AMI" a lot during this process. It stands for Area Median Income. In simple terms, it is the middle-of-the-road income for families in your county.

For Hawaiʻi County (Big Island), the 2025 median family income is $98,800 per year for a family of four. When we say "60% AMI," that means 60% of that number, which is about $59,280 for a family of four.

Why does this matter? Because the federal programs that help pay for building these homes require that the homes go to families within certain income ranges. Each lot has an income limit based on which program pays for it.

Income Limits by Household Size

Find your household size in the left column. Then look across to see the maximum income for each tier:

| Family Size | 30% AMI | 50% AMI | 60% AMI | 70% AMI | Market Rate |

|---|---|---|---|---|---|

| 1 person | $25,410 | $42,350 | $50,820 | $59,290 | No limit |

| 2 people | $29,040 | $48,400 | $58,080 | $67,760 | No limit |

| 3 people | $32,670 | $54,450 | $65,340 | $76,230 | No limit |

| 4 people | $36,270 | $60,450 | $72,540 | $84,630 | No limit |

| 5 people | $39,180 | $65,300 | $78,360 | $91,420 | No limit |

| 6 people | $42,090 | $70,150 | $84,180 | $98,210 | No limit |

Source: HUD FY2025 Income Limits, Hawaiʻi County. These numbers are updated every year. The limits used will be whatever HUD has published at the time your income is certified.

How You Get Assigned to a Bucket

After your income is verified by a third-party certifier, you are placed into one of four "buckets" based on how much your household earns:

Bucket A — 30% AMI or less

You can choose from any lot — all 125 are available to you. You have the most options.

Bucket B — Between 31% and 60% AMI

You can choose from 50%, 60%, 70% AMI lots, and market rate lots. That is 110 lots available.

Bucket C — Between 61% and 70% AMI

You can choose from 70% AMI lots and market rate lots. That is 54 lots available.

Bucket D — Over 70% AMI

You can choose from the 25 market rate lots only. These are immediate ownership — no rental period.

The important rules to know:

Lower income CAN select higher-tier lots. If you qualify at 30% AMI, you can still choose a 60% or 70% lot if you prefer. You are not locked into the lowest tier.

Higher income CANNOT select lower-tier lots. If you qualify at 70% AMI, you cannot choose a 30% or 60% lot. Those are reserved for families with lower incomes.

If you earn too much for RWOTP and there are no market rate lots left, you are deferred. This means you go back to the DHHL waitlist and wait for the next offering. You do NOT lose your spot on the list. You are deferred, not removed.

A note about blood quantum vs. income

Your DHHL eligibility (50% Hawaiian blood quantum) is separate from your income qualification. These income limits come from the federal housing programs (LIHTC and NAHASDA), not from the Hawaiian Homes Commission Act. Being over-income does not affect your status as a DHHL beneficiary.

The Lot Selection Meeting & Your Questions

What Happens at the Lot Selection Meeting

Here is what the meeting looks like, step by step:

A big map of all 125 lots is displayed

The map is color-coded. Red lots are 30% AMI, blue lots are 60% AMI, green lots are 70% AMI, and gold lots are market rate. You can see at a glance which ones are available to you.

Names are called in waitlist order

The oldest application date goes first. This is strict — the order comes from the DHHL master waitlist. There are no exceptions.

Your income bucket is confirmed

When your name is called, the staff will confirm your bucket (A, B, C, or D). This tells everyone which lots you are eligible to choose from.

You walk up and choose your lot

You go to the map and place a sticker on the lot you want from your eligible options. Your choice is final, so take a moment to decide. Look at the location, the neighbors, the orientation.

The next person is called

If there are no eligible lots left for someone, they are deferred — they keep their waitlist position and wait for the next DHHL project.

You sign your agreement

If you chose an RWOTP lot, you sign a rental agreement. If you chose a market rate lot, you sign a homestead lease and mortgage documents. Then you move toward your new home.

Your Questions Answered

This is your opportunity. Your ʻāina. Your future.

If you have more questions, please ask the DHHL or Kalanianaole Development staff at the orientation. We are here to help you through every step.